VIX Spread Trade Still Has The Pit Buzzing

By Russell Rhoads, CFA

Things are fairly quiet today in the equity markets and the VIX

pit, but traders are still talking about a pretty interesting

spread

that was initiated on Tuesday. A trader came in and sold 25,000 VIX Sep

17 Calls and subsequently purchased

200,000 VIX Sep 27 Calls for a net

cost of 0.02 (two cents to clarify the decimal was not misplaced) or in

real dollar

terms a cost of $50,000. In textbook terms this is a 1 by 8

Call Backspread. It trader terms this is a, “I expect (or hope)

VIX

runs to the 30’s between now and September 18th” which is

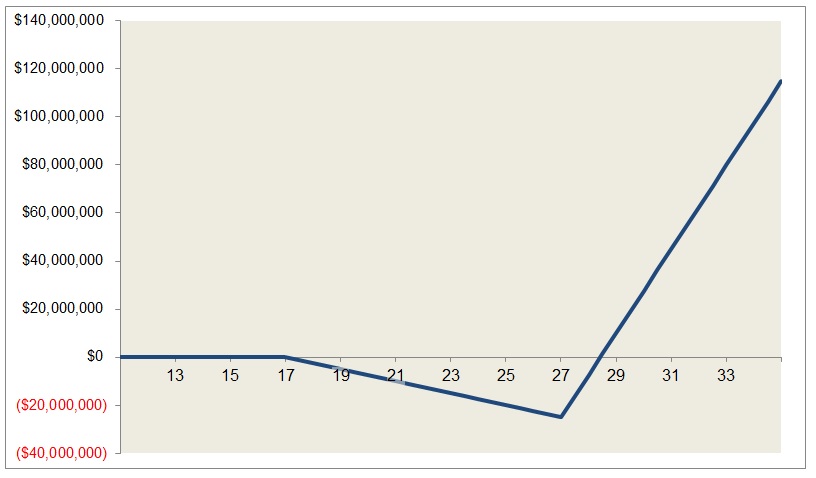

expiration date for VIX futures and options. The payoff

diagram shows

why VIX in the 30’s would be a good outcome for this spread trade.

VIX is just a bit under 16.00 today which at expiration would result

in both legs of this spread expiring with no value and

the trader being

out the premium paid for the trade. A worst case scenario for this

trade involves VIX rallying but only

to 27.00 at expiration. This worst

possible outcome would result in a loss of $25,050,000. That’s because

the short

position in 25,000 of the VIX Sep 17 Calls would be 10 points

in the money. In math terms it is $10.00 x 100 x 25,000

or $25,000,000

plus the $50,000 cost of initiating the trade. The breakeven point is a

fraction of a cent over 28.43.

Above this level the trade makes

$175,000 for each 0.01 VIX move to the upside. Odds are this trade

would not make

it to expiration in the case of a rally, but we will have

to wait and see over the next couple of weeks.